Transcribed

Papua New Guinea : Private sector credit growth and bank lending margin

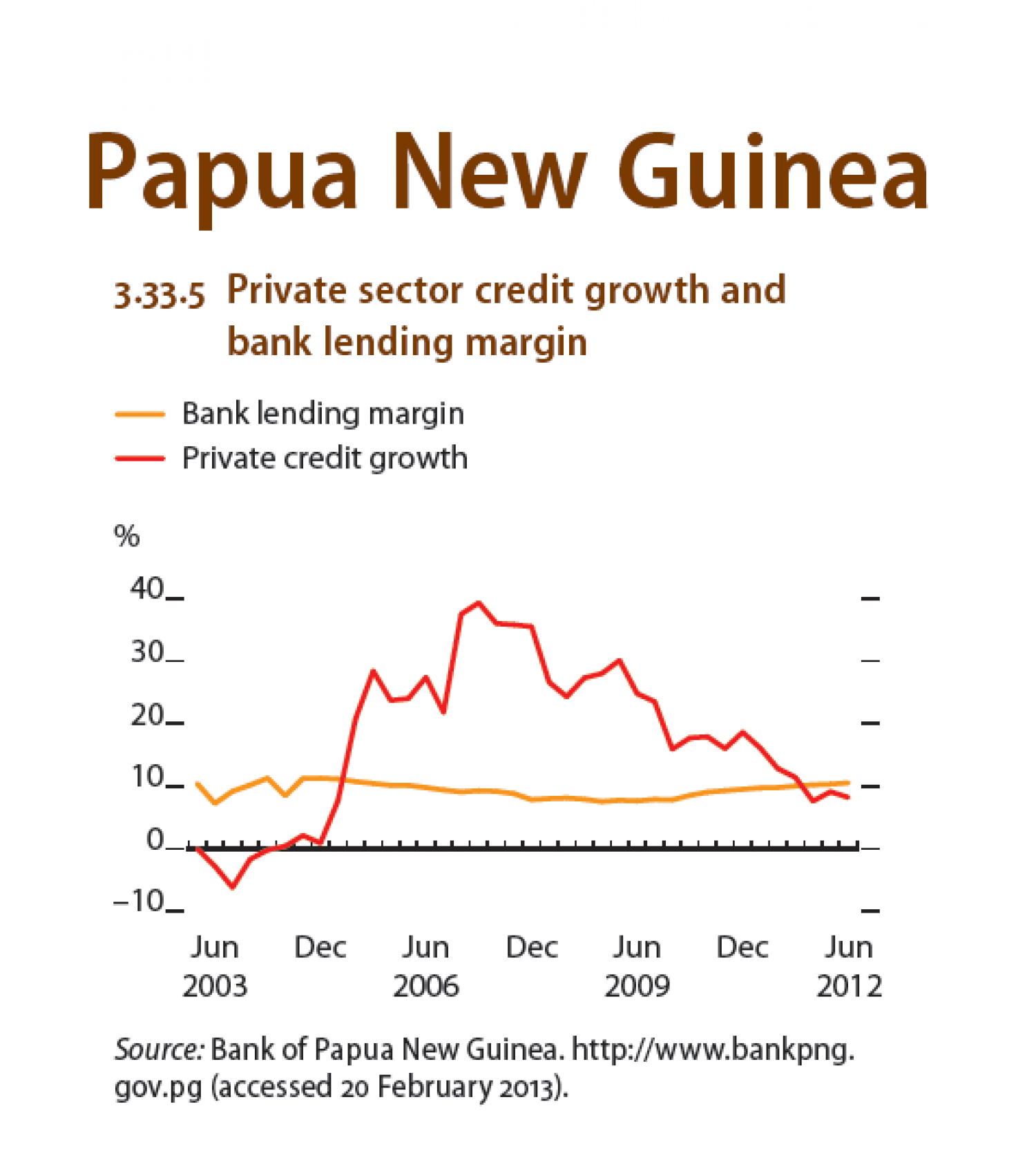

Papua New Guinea 3.33.5 Private sector credit growth and bank lending margin Bank lending margin Private credit growth 40_ 30_ 20- 10_ -10_ Jun Dec Jun Dec Jun Dec Jun 2003 2006 2009 2012 Source: Bank of Papua New Guinea. http://www.bankpng. gov.pg (accessed 20 February 2013).

Papua New Guinea : Private sector credit growth and bank lending margin

shared by PARMIONOVA on Apr 26

198

views

0

faves

0

comments

In response to lower inflation, the central bank lowered its target

interest rate from 7.75% to 6.75% in September 2012, signaling easing

monetary policy intentions. However, with the central bank una...

ble to

fully absorb the high liquidity in the commercial banking system, the

impact of target interest rate movements on market interest rates and

inflation continued to be limited. Private sector credit growth remained

near 10% per annum during 2012, well off its peak of 40% in 2007

(Figure 3.33.5).

Economic growth is expected to slow to 5.5% in 2013 before picking up

again to 6.0% in 2014. The non-mineral economy is expected to slow

most sharply as the winding down of LNG project construction will

dramatically curtail construction and transport activity, eventually

spilling over into lower domestic consumption and retail and wholesale

trade. Moderating international agricultural prices are expected

to depress rural incomes derived from the sale of crops for export.

A significantly increased national budget, which plans for large budget

deficits of 7.2% of GDP in 2013 and 5.9% in 2014, will counter some of the

effects of falling domestic demand on the non-mineral economy.

The mineral sector is expected to lead growth, expanding by 13.0%

in 2013 as production bottlenecks clear at a number of gold and copper

mines and production at the new Ramu nickel and cobalt mine ramps

up. Continued declines in petroleum production, as reserves in major oil

fields become depleted, will offset some of this growth in 2013, but the

onset of LNG exports will greatly boost mineral output late in 2014, with

overall growth in the sector expected to surpass 60% in that year.

In 2013, an expected easing of the kina exchange rate could fuel

resurgence in imported inflation, while high government spending is

likely to stoke domestic inflation. The winding down of LNG plant

construction will be a counterinfluence subduing price growth later

in 2013 and throughout 2014. This period will see up to 8,000 workers

demobilized, easing a shortage of skilled labor and other private

sector capacity constraints, particularly in construction and transport.

Declining capital imports associated with the LNG project will relieve

port congestion. On balance, inflation is projected to bounce back to 6.5%

in 2013 and 7.5% in 2014.

The 2013 current account deficit is expected to narrow to 15.1% of GDP

as reduced LNG capital imports reduce the trade deficit. A rebound in

production at existing mines and the ramping up of production at the

Ramu facility will help boost export earnings. A further narrowing of the current account deficit to 8.4% of GDP is expected in 2014 as LNG exports begin

Source: Bank of Papua New Guinea. http://www.bankpng.gov.pg (accessed 20 February 2013)

Source

http://www.bankpng.gov.pgCategory

EconomyGet a Quote