My Employer's Health Coverage Vs. Obamacare

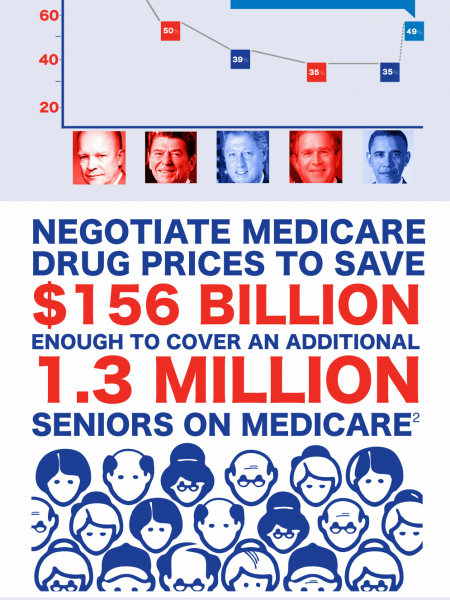

MY EMPLO YER'S HEALTH COVERAGE v. ОВАМАСАRE HEALTH CARE COVERAGE IN THE U.S. AFFORDABLE OPEN CARE ACT ENROLLMENT THE AFFORDABLE CARE ACT (ACA), OR "OBAMACARE," OBAMACARE'S FIRST OPEN ENROLLMENT PERIOD RAN WAS SIGNED INTO LAW BY PRESIDENT BARACK FROM OCTOBER 1, 2013 TO MARCH 31, 2014 OBAMA ON MARCH 23, 2010 As of Oct. 2014, 6.7 million Americans (about Obamacare created the Health Insurance 2.1% of the population) have signed up for Marketplace (also called the Exchange), full health care coverage under Obamacare which refers to each state's price comparison THE SECOND OPEN ENROLLMENT PERIOD FOR OBAMACARE website for subsidized health insurance RUNS FROM NOVEMBER 15, 2014 TO FEBRUARY 15, 2015 The Marketplace is the only place to receive It is estimated that 9 to 10 million Americans will cost assistance for Americans making less have signed up by the end of this period than 400% of the federal poverty level KEY STATISTICS (AMERICANS) RECEIVING RECEIVING RECEIVING RECEIVING YEAR HEALTH PRIVATE HEALTH EMPLOYMENT-BASED GOVERNMENT HEALTH UNINSURED INSURANCE (%) INSURANCE (%) HEALTH INSURANCE (%) INSURANCE (%) (%) 2006 84.8 68.7 60.3 27.1 15.2 2007 85.3 68.2 59.8 27.8 14.7 2008 85.1 67.2 58.9 29.1 14.9 2009 83.9 64.5 56.1 30.6 16.1 2010 (ACA) 83.7 64.0 55.3 31.3 16.3 2011 84.3 63.9 55.1 32.2 15.7 2012 84.6 63.9 54.9 32.6 15.4 2013 86.6 64.2 53.9 34.3 13.4 UNDERSTANDING NEW CONSUMER RIGHTS AND PROTECTIONS ESSENTIAL BENEFITS Starting in 2014, all private health insurance plans offered in the Marketplace must include items and services within at least the following 10 categories: AMBULATORY PATIENT SERVICES EMERGENCY SERVICES MATERNITY AND NEWBORN CARE MENTAL HEALTH AND SUBSTANCE USE DISORDER SERVICES HOSPITALIZATION PRESCRIPTION DRUGS REHABILITATIVE AND HABILITATIVE SERVICES AND DEVICES LABORATORY SERVICES PREVENTIVE AND WELLNESS PEDIATRIC SERVICES, SERVICES AND CHRONIC DISEASE MANAGEMENT INCLUDING ORAL AND VISION CARE OTHER RIGHTS AND PROTECTIONS In addition to the 10 essential benefits, all private health insurance plans must have the following characteristics: • INSURERS MUST AT LEAST 60% OF OUT-OF-POCKET COSTS ON REQUIRED SERVICES YOU CANNOT BE DENIED COVERAGE FOR ANY REASON OTHER THAN THE ABILITY TO PAY YOU MUST BE ABLE TO RENEW THE POLICY REGARDLESS OF HEALTH STATUS • THERE ARE LIMITS TO THE AMOUNT YOU CAN BE CHARGED BASED ON AGE, TOBACCO USE, FAMILY SIZE AND GEOGRAPHY INSURERS CANNOT PLACE DOLLAR LIMITS ON THE 10 ESSENTIAL BENEFITS YOUNG ADULTS If you have an individual or employment-based plan (with minimum essential coverage) that covers children, you can add or keep your children on your health insurance policy until they turn 26 years old This applies even to young adults who are: V MARRIED V NOT LIVING WITH THEIR PARENTS V ATTENDING SCHOOL V NOT FINANCIALLY DEPENDENT ON THEIR PARENTS V ELIGIBLE TO ENROLL IN THEIR EMPLOYER'S PLAN NAVIGATING THE NEW HEALTH CARE LANDSCAPE INDIVIDUAL MANDATE If you or your dependents don't have insurance that qualifies as minimum essential coverage in 2014, you'll pay the higher of these two amounts when you file your 2014 federal tax return: • 1% OF YOUR YEARLY HOUSEHOLD INCOME (above the tax filing threshold) The maximum penalty is the national average premium for a Bronze plan • $95 PER PERSON FOR THE YEAR ($47.50 per child under 18) The maximum penalty per family using this method is $285 The penalty increases every year. In 2016 it will be 2.5% of income or $695 per person If you're uninsured for more than three months of the year, you have to pay 1/12 of the yearly penalty for each month you're uninsured EMPLOYER MANDATE All businesses with over 50 full-time equivalent (FTE) employees must provide health insurance for their full-time employees, or pay a per month penalty on their federal tax returns • 96% OF ALL FIRMS IN THE U.S. ( 5.8 MILLION OUT OF 6 MILLION TOTAL FIRMS) have under 50 FTE employees and will not be penalized for choosing not to provide health coverage to their employees To meet the minimum value requirement, an employer-sponsored plan must cover at least 60% of total allowed costs - i.e., what the plan pays versus what the customer pays due to deductibles, copays and coinsurance The annual penalty is $2,000 per employee if insurance isn't offered PART-TIME WORKERS Employers aren't required to provide health insurance for part-time employees, even if they provide coverage for full-time employees • IF YOUR EMPLOYER DOES NOT PROVIDE YOU WITH HEALTH COVERAGE FOR ANY REASON, YOU CAN USE THE HEALTH INSURANCE MARKETPLACE TO BUY SUBSIDIZED QUALITY HEALTH INSURANCE According to one argument, many medium-size and large employers are pushing workers into part-time jobs as a way to get around the "employer mandate" UNEMPLOYED Regardless of your employment status, you must have minimum essential coverage or pay a fee. Your household size and income, not your employment status, determine what health coverage you're eligible for and how much help you'll get paying for coverage If you're unemployed, you may qualify for the following: • MEDICAID • CHILDREN'S HEALTH INSURANCE PROGRAM (CHIP) • PRIVATE HEALTH INSURANCE THROUGH THE MARKETPLACE GRANDFATHERED PLANS Grandfathered plans are those that were in existence on March 23, 2010 and haven't been changed in ways that substantially cut benefits or increase costs for consumers Job-based grandfathered plans can enroll people after March 23, 2010 and still maintain their grandfathered status Grandfather plans don't have to: • Cover preventive care for free • Guarantee your right to appeal a coverage decision • Protect your choice of doctors and access to emergency care • Be held accountable through rate review for excessive premium increases CHOOSING A PLAN ACCEPTED PLANS Remember, you don't have to buy a plan through the Marketplace. You can buy it directly from an insurance company, from a commercial online service, or through an agent or broker. As long as it offers the minimum essential coverage, you will not have to pay a penalty EMPLOYER HEALTH CARE TYPES • Health Maintenance Organization (HMO) • High-Deductible Health Plan with Savings Option (HDHP/SO) • Health Savings Account (HSA) • Preferred Provider Organization (PPO) • Point of Service (POS) COSTS AVERAGE MONTHLY AND ANNUAL PREMIUMS FOR EMPLOYER-SPONSORED 2014 HEALTH INSURANCE, SINGLE AND FAMILY COVERAGE BY PLAN TYPE MONTHLY ANNUAL HMO Single Coverage $519 $6,223 Family Coverage $1,449 $17,383 PPO Single Coverage $518 $6,217 Family Coverage $1,444 $17,333 POS Single Coverage $514 $1,336 $6,166 $16,037 Family Coverage HDHP/SO Single Coverage $442 $1,283 $5,299 Family Coverage $15,401 ALL PLAN TYPES $502 $1,403 Single Coverage $6,025 $16,834 Family Coverage MARKETPLACE HEALTH CARE The SHOP will offer employers a choice of four categories of insurance packages, each with essential minimum benefits. Employers will decide what level of coverage to offer, and employees may pick any plan offered within the exchange at the employer's chosen coverage level BRONZE YOUR HEALTH PLAN PAYS 60% ON AVERAGE - YOU PAY ABOUT 40% SILVER YOUR HEALTH PLAN PAYS 70% ON AVERAGE - YOU PAY ABOUT 30% GOLD YOUR HEALTH PLAN PAYS 80% ON AVERAGE - YOU PAY ABOUT 20% PLATINUM YOUR HEALTH PLAN PAYS 90% ON AVERAGE - YOU PAY ABOUT 10% COSTS 2014 AVERAGE MONTHLY AND ANNUAL PREMIUMS BY AGE AND PLAN TYPE 30 40 50 60 BRONZE Monthly $263 $296 $413 $627 Annual $3,156 $3,552 $4,596 $7,524 SILVER Monthly $284 $319 $447 $678 Annual $3,408 $3,828 $5,364 $8,136 GOLD Monthly $336 $378 $528 $801 Annual $4,032 $4,536 $6,336 $9,612 PLATINUM Monthly $345 $388 $543 $825 Annual $4,140 $4,656 $6,516 $9,900 MORE INFORMATION INDIVIDUAL FEES healthcare.gov/fees-exemptions/fee-for-not-being-covered INDIVIDUAL EXEMPTIONS healthcare.gov/fees-exemptions/exemptions-from-the-fee ACCEPTED PLANS healthcare.gov/fees-exemptions/plans-that-count-as-coverage OVERVIEW OF SHOP MARKETPLACE healthcare.gov/small-businesses/provide-shop-coverage/shop-marketplace-overview STATS ON MARKETPLACE PLANS healthpocket.com/healthcare-research/infostat/medical-use-age-obamacare-plan-choice#.VG7fQvnF-Sq DETAILED FACTS ABOUT OBAMACARE ObamacareFacts.com HOW WILL OBAMACARE AFFECT ME? obamacarefacts.com/how-will-obamacare-affect-me DETAILED INFO ABOUT SMALL BUSINESS COVERAGE healthcoverageguide.org UNEMPLOYED healthcare.gov/unemployed UNDERSTANDING HEALTH INSURANCE healthinsurance.about.com/od/healthinsurancebasics/a/Hmo-Ppo-Epo-and-Pos-whats-The-Difference-and-Which-ls-Best.htm |UNIVERSITY of UF FLORIDA pharmd.distancelearning.ufl.edu Sources http://www.census.gov/hhes/www/hlthins/data/historical/HIB_ tables.html http://www.census.gov/hhes/www/cpstables/032014/health/h01_000.htm http://www.bloomberg.com/news/2014-11-20/obamacare-s-subscriber-rolls-include-unpublicized-dental-plans.html http://www.nationaljournal.com/health-care/hhs-lowers-expectations-for-obamacare-enrollment-20141110 http://www.census.gov/content/dam/Census/library/publications/2014/demo/p60-250.pdf http://cnsnews.com/news/article/obamacare-mandate-anyone-who-works-30-hour-week-now-full-time http://www.forbes.com/sites/dandiamond/2014/09/04/part-time-jobs-are-increasing-but-dont-blame-obamacare-yet/ http://kaiserfamilyfoundation.files.wordpress.com/2014/09/8625-employer-health-benefits-2014-annual-survey4.pdf http://www.healthpocket.com/healthcare-research/infostat/medical-use-age-obamacare-plan-choice#.VG7LU_nF-Sp http://obamacarefacts.com/ https://www.healthcare.gov/ http://healthinsurance.about.com/od/healthinsurancebasics/a/Hmo-Ppo-Epo-and-Pos-whats-The-Difference-and-Which-Is-Best.htm http://healthcoverageguide.org/

My Employer's Health Coverage Vs. Obamacare

Source

http://pharm...obamacare/Category

HealthGet a Quote