U.S. Retirement Challenges

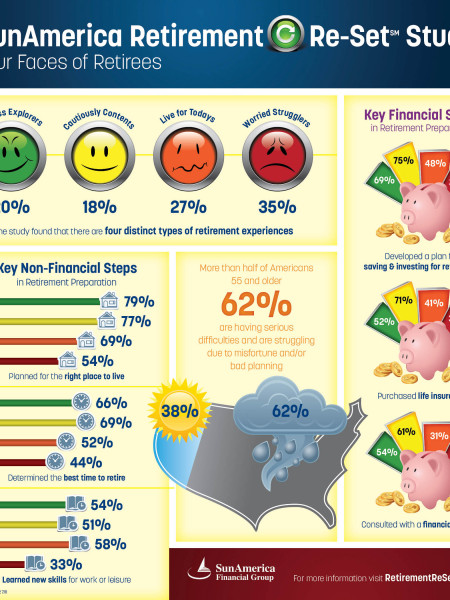

PRB INPORM IMPOWER ADVANCE US. RETIREMENT CHALLENGES MORE PEOPLE ARE LIVING LONGER INDIVIDUALS MUST PLAN and save for longer retirement spans, working lives, or both. Policymakers are confronting fiscal pressure to modify Social Security and other programs for older Americans. The ratio of A larger share of the population is reaching age 65. workers to retirees is shrinking. BIRTH YEAR • 2000 • 1950 • 1900 BY 2040, THERE WILL BE 91% ABOUT 2 WORKERS 86% CONTRIBUTING TO SOCIAL SECURITY FOR EACH RETIRE 85% 76% 58% 479 1960|1 to 5 RATIO MEN WOMEN More people can expect to live longer after 65. O AVERAGE AGE OF DEATH AFTER 65 O AGE AT WHICH 1 IN 5 WILL STILL BE LIVING PRESENT| 1 to 3 RATIO 1900 79 1950 83 2000 85 93 2040| 1 to 2 RATIO 1900 83 92 1950 85 93 2000 85 96 60 70 80 90 100 AGE A LARGE SHARE OF OLDER AMERICANS RELY MAINLY ON SOCIAL SECURITY CHANGES TO SOCIAL SECURITY benefits will have the biggest impact on those with below-average incomes. Below-Average Incomes LOWEST UPPER - MIDDLE AVG. ANNUAL 85% INCOME $6,800 57% AVG. ANNUAL INCOME $26,600 LOWER - MIDDLE HIGHEST AVG. ANNUAL INCOME $15,400 AVG. ANNUAL 84% 18% INCOME $78,200 • EARNINGS • PENSION INCOME • OTHER INCOME AGES 65 AND OLDER 2013, BY INCOME GROUP PUBLIC ASSISTANCE/SSI SOCIAL SECURITY ASSET INCOME A SIZEABLE GROUP IS AT RISK OF NOT SAVING ENOUGH Employers have increasingly shifted from offering defined benefit (DB) pension plans to defined contribution (DC) retirement savings plans that require individuals to make complex long-term investment decisions. As a result, more people may be at risk of not saving adequately. Defined Benefit (DB) Defined Contributlon (DC) Individual Retirement Account (IRA) GUARANTEED Pension plans with guaran- teed payouts based on years worked and pay level. Retirement savings plans (like 401Ks); amount avail- able for retirement depends on contribution levels and investment performance Personal accounts that employed people can open to make tax-deductible contributions to their retirement savings. over time. Older Americans without defined benefit pensions have fewer retirement resources. Household average balance by savings vehicle(s), 55-64 age group, 2010 DC + DB + IRA $545,000 DB + IRA $364,000 DC + DB $237,000 DB $205,000 DC + IRA $185,000 IRA $46,000 DC $26,000 • DEFINED CONTRIBUTION (DC) • DEFINED BENEFIT (DB) • INDIVIDUAL RETIREMENT ACCOUNT (IRA) Who is most likely to be inadequately prepared? 20% 35% 49% %3D MARRIED COUPLES SINGLE MEN SINGLE WOMEN 649 38% 32% NO HIGH SCHOOL DIPLOMA HIGH SCHOOL DIPLOMA COLLEGE DEGREE OR MORE PERCENT INADEQUATELY PREPARED, AGES 66 TO 69, 2008 THERE IS NO ONE-SIZE-FITS-ALL RETIREMENT POLICY Low Income Middle Income High Income Could be encouraged to save more; would benefit from expanded access to retirement savings mechanisms. Have access to a wide range of defined contri- bution (DC) savings opportunities. Personal saving is difficult; Social Security will be crucial. SOURCE: James Poterba, "Retirement Security in an Aging Population," American Economic Review: Papers & Proceedings 104, no. 5 (2014): 1-33. Also see: Felicitie Bell and Michael Miller, "Life Tables for the United States Social Security Area 1900-2100," U.S. Social Security Administration Actuarial Study 120 (2005); and Michael Hurd and Susann Rohwedder, "Economic Preparation in Retirement," in Investigations in the Economics of Aging, ed., David Wise (Chicago: University of Chicago Press, 2012): 77-113. ©2014 Population Reference Bureau. All rights reserved. BIRTH YEARS WOMEN MEN

U.S. Retirement Challenges

Publisher

Population Reference BureauSource

http://www.p...urity.aspxCategory

EconomyGet a Quote