It's All Connected: An Overview of the Euro Crisis

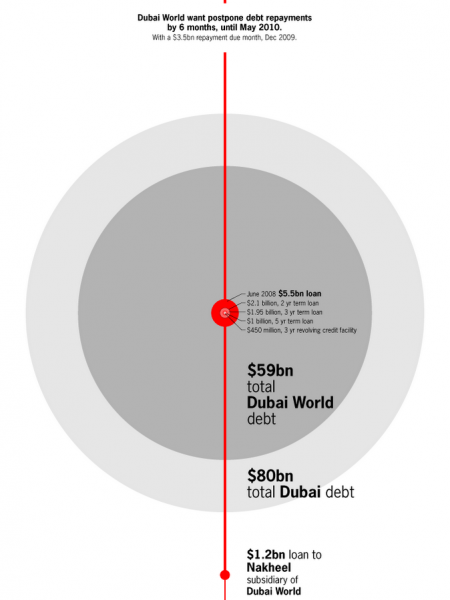

DATA POINTS BILL MARSH It's All Connected: A Spectator's Guide to the Euro Crisis Charting the web of debt exposure among sagging economies. Arrows show imbalances of debt exposure between countries. Arrows point from debtors to their bank creditors; arrow widths are proportional to the balance of money owed. (Figures, released last week, are from June 2011, in billions of dollars.) For example, French borrowers owe Italian banks $50.6 billion; Italian borrowers owe French banks $416.4 billion. The difference their imbalance – shows France's banking system more exposed to Italian debtors by about $365.8 billion. There is no complete accounting of debt between countries. The Bank for International THE COLOR OF TROUBLE COMPARISON OF ECONOMIES Circle sizes HOW TO READ THIS Spain The risk to countries' debts and economies is indicated by color: indicate the scale of each country's gross domestic product, in dollars. Settlements compiles the most detailed data, listing amounts that banks based in one country are exposed to by debtors in other countries, both government and private. CHART G.D.P. $1.4 TRILLION SCALE OF GOVERNMENT INDEBTEDNESS 56% Each country's gross government debt as a percentage of its G.D.P., as tallied by the International Monetary Fund. More worrisome NHE global financial system is highly interconnected. So problems in one part German Eyes on Italy Although German debtors owe Italian banks more than Italians owe German banks, the latter is still a huge sum: ... And Reach ) American Shores ... American lenders and money-market funds are already moving their money out of European banks, which are balking at lending to one another, writes Kotlikoff. "This is exactly happened before the bankruptcy of Lehman Brothers Holdings Inc. in 2008," he adds. American banks are heavily exposed to Spain, Ireland and Italy. (American banks' exposure to Greece is smaller and less direct.) On top of this, Ameri- can exports to the European Union collectively the biggest American trading partner - could suffer if the crisis slowed European growth and caused the euro to depreciate against the dollar. $161.8 billion. of the world can reverberate the economist Laurence what almost everywhere else – risking a cascade of default, contagion, contracting credit and collapsing economic activity. Exhibit A now is Germany Struggling to Stay on Top French support of bailouts and its banks could add to its liabilities. Last week Moody's warned of a downgrade to France's sterling credit rating. France Bill Marsh is a graphics editor at The New York G.D.P. $3.3 TRILLION $53.8 G.D.P. $2.6 TRILLION 83% 87% Times. $17.3 $323.9 $321.5 $53.9 Europe. $19.3 $7.7 European Union leaders are $321.2 $32.5 $118.1 $18.6 meeting this week to at last deal with a debt crisis rattling $117.6 The Epicenter: Greece $48.9 $365.8 investors worldwide who once G.D.P. $0.3 TRILLION thought lending to euro zone countries was virtually risk-free. The graphic here Italy: France's Worry ......... 166% Unless Bailouts 6 Äre Big Enough . Debtors in the helps you see the intertwined complexities. Germany and Ireland Total German bank exposure to Irish debt is a significant $110.5 billion. euro zone's third largest economy owe the banks of its second largest economy a total of $416.4 billion, equivalent to about one-fifth of Italian G.D.P. The troubled euro zone could, by some estimates, require about $1.3 trillion to $2.06 trillion in bailouts – an amount perhaps bigger than the Spanish G.D.P. or more than half the size of the German economy. The bailout fund set up last year by euro zone countries goes ungainly title of European Financial Stability Facility. The fund has only about $600 billion on hand. Here are total European bank exposures to the five most distressed economies, accord- ing to the Bank for International Settle- ments, compared with the size of each economy: $111.1 1 It Starts With The Euro ... Ireland Italy Britain and Ireland What they owe each other's banks is nearly identical, masking British bank exposure to Irish debt in this chart. Irish borrowers owe British banks $140.8 billion. s0.3 G.D.P. $0.2 TRILLION G.D.P. $2.1 TRILLION In 1999, most countries in the European Union adopted the euro as a common currency. This union allowed poorer countries like Portugal, Italy, Ireland, Spain and Greece to borrow money at the same low interest rates as rich and financially prudent Germany, even though their inflation rates were higher. That gave them a strong incentive to borrow. 109% 121% $12.0 The Shaky Five $0.9 4 EQUIVALENT PERCENT OF EACH COUNTRY'S G.D.P. $1.4 $88.5 $38.8 $22.4 Japan $0.6 Italy $837.5 BILLION 41% 2 : And Goes Bad In Greece ... G.D.P. $5.5 TRILLION $0.8 Spain $643.2 46 ... 233% $26.0 Britain Ireland $380.1 184 $10.1 G.D.P. $2.3 TRILLION Spain $18.9 Portugal $196.7 86 Greece financed a large public-welfare state and built up huge debt for its size that it has scant hope of repaying now. In 2010, European financial institutions began bailing out Greece (later Ireland and Portugal, too); lenders were prodded to agree to modest, voluntary debt write-downs, or "haircuts." But Greece still needs money. And its credit bill grows ever larger as lenders charge more and demand government cutbacks, which in turn have provoked civil unrest. After years of propping up the spendthrift Greeks, the Germans are fed up. The problem is, a chaotic Greek default could hurt all European banks and pension funds that have extended Greece credit down the years, and maybe cause a wider bank panic. So bailouts continue – for now, at least: G.D.P. $1.4 TRILLION $9.8 Although it has more than twice its G.D.P. in government debt, most of that debt is owed internally, not to outside creditors. So Japan is not considered a default risk. Greece $120.8 40 81% $3.8 106% $2.2 56% $325.8 TOTAL $2.178 TRILLION $19.4 $62.0 Portugal: Spain's Worry $0,5 G.D.P. $0.2 TRILLION Its debtors owe Spanish banks a total of $88.5 billion, equivalent to 39 percent of Portuguese G.D.P. $25.9 $163.0 One of Many I Crisis Unknowns $344.8 $795.2 $28.2 Bank secrecy, government secrecy, a paucity of global financial statistics: all contribute to large information voids that leave experts uncertain. Here is a sampling. U.S. Risk $3.1 Total American bank exposure to ... Spanish debt: $66.8 billion Irish debt: Italian debt: $11.1 $3.2 $53.6 $46.9 WHO'S EXPOSED TO BAD DEBT? Some banks are more forthcoming than others – there is no consistent disclo- sure. American money market funds are thought to have significant invest- ment in European banks. So-called stress tests of big banks earlier this year are now widely believed to have understated the level of bank risk. Meanwhile, banks say they have been struggling to lessen their exposure to bad debt. United States G.D.P. $14.5 TRILLION 100% BEST CASE Bailouts in the form of new European credit eventually work. Greece pays down its hefty debts with a combination of growth and continued domestic austerity for years to come. The United States has its own debt troubles, and political squabbling over its debt ceiling led to a historic downgrade of its credit rating. But in the context of Europe, things aren't so bad. ? ? MORE LIKELY Bailouts don't work. Greek debt grows in an anemic or shrinking economy. The country defaults, either in a negotiated, orderly manner or chaotically, forcing lenders to take big losses either way. But damage could be contained if countries in the euro zone can erect a financial firewall to backstop the credit of the four other shaky nations: Ireland, Portugal, Spain and Italy. This is what the European Union is trying to agree on this week, as France prods a more reluctant Germany. What euro zone borrowers owe China is not known. "The U.S. has high debt but we are the presumed safe haven, so capital would flood into the U.S. if the euro zone goes really badly," said Simon Johnson of M.I.T., a former chief economist at the International Monetary Fund. WHO INSURED BAD DEBT? Banks and hedge funds sell insurance against investor losses from default by their borrowers. These “bets" that losses won't occur are called credit default swaps. With defaults in Greece and elsewhere a real possibility, issuers of these swaps could be on the hook for losses that once seemed unlikely. How those billions would be covered is unknown; who, precisely, insured Greek debt is also unknown. China: China holds about $1.5 trillion in U.S. debt, mostly Treasury debt. There are no known significant American holdings of Chinese debt. The Great Unknown G.D.P. $5.9 TRILLION ? WORST CASE? See below. WHERE ARE THESE ECONOMIES HEADED? Signs are not good. Some economists argue that measures being put in place to cut public debt also dampen economic growth: a hobbled private sector is not hiring, and now neither is the govern- government austerity Threatening ) Contagion . That Could 4 Unfold Quickly .. ... Its foreign currency reserves total more than $3 trillion. If the firewall fails to materialize, or inspire investor confidence, or proves inadequate, it would be easy to imagine a run on banks, because the single currency makes it easy to shift money across borders from risky economies to safer ones. That and the lack of central If nothing is done to prevent it, a chain of events like this one, involving countries on the large chart above, could unfold: GREECE DEFAULTS In reaction, investors become more concerned about their exposure to other risks in the region, especially the other four most troubled economies. Borrowing costs rise for Ireland, Italy, Portugal and Spain, adding to their debt loads. MONEY TAKES FLIGHT Investors fear that richer creditor nations may not bail out other shaky countries. And given the ease of shifting money across borders in the euro zone, a flood of money from risky economies to safer ones like Germany can take place in a matter of hours. FRANCE NEXT? Meanwhile, the Italian government, barely solvent, is unable to protect domestic banks if there is a loss of confidence in them. French banks, heavily burdened with all manner of Italian debt, totter. Exposure to French banks could lead to losses beyond the Continent. ment. A slow economy generates less in taxes; the debt - which doesn't go away unless there's a default – is not paid down. "When you have a financial crisis, growth is slow for a long time," Mr. Rogoff said. banks in each country away with the arrival of the euro - make the euro zone "the ultimate contagion machine," said Kenneth Rogoff, the Harvard economist and co-author of "This Time Is Different: Eight Centuries of Financial Folly." those went HOW MUCH IS CHINA OWED? Chinese exposure can only be guessed; whether China will participate in bailouts is uncertain. The same holds true for other big global creditors like Saudi Arabia and other petro-states. GERMANY FRANCE GREECE EURO ZONE ITALY: IRE. ITALY Seth W. Feaster, Nelson D. Schwartz and Tom Kuntz contributed reporting. JAPAN SPAIN PORT, Note: The B.I.S. data used here do not include debts between non-bank entities. Figures show amounts that bank systems, based in or controlled from one country, are exposed to debts from borrowers in other countries. U.S. Sources: Bank for International Settlements (bank exposure data; table 9D of Preliminary International Banking Statistics Report, released Oct. 20, at www.bis.org): Simon Johnson, Massachusetts Institute of Technology: Kenneth S. Rogoff, Harvard University: International Monetary Fund (G.D.P. size and general government debt- to-G.D.P. ratios); Congressional Research Service (American bank exposure) THE NEW YORK TIMES

It's All Connected: An Overview of the Euro Crisis

Source

Unknown. Add a sourceCategory

EconomyGet a Quote